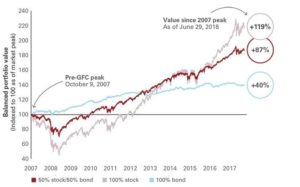

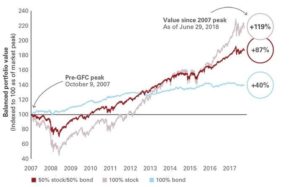

Now is a good time to learn the lessons from the Global Financial Crisis

As we hit the 10-year anniversary, there are lessons to learn from the economic challenges and 2nd worst market in history, and subsequent recovery, that began a decade ago. 10 years is long enough that some people don’t even remember this major financial event, while others feel like they are still recovering, given that the economy’s recovery has been gradual, even though the market’s recovery has been strong… maybe a bit too strong. The takeaway is that staying the course and being a disciplined investor is highly valuable. The chart below indicates that it took only approximately 1 year for a 50/50 stock/bond mix to recover from the bottom, and about 2 years from the prior peak.

If you were early in your career and retirement savings process, you had time to ride out the storm and feel the recovery. If you were just starting retirement and had a stock/bond mix that was not appropriate for your life stage, it was likely difficult to fully recover, especially if you needed to begin spending. Using the right stock/bond mix along all stages of life helps avoid those problems, especially if you save the appropriate amount each year.

Millennials, who are often more sensitive to risk than their Baby Boomer parents because the Global Financial Crisis was their first investment experience, often now invest more conservatively than is typically recommended for their age. That’s not necessarily a bad thing, if offset by the right increase in savings to offset the lower expected growth from a lower volatility (i.e. read less stocks, more bonds) portfolio, but some won’t be able to save enough to make up for that difference. In that case, it is important to explore getting more comfortable with taking an appropriate level of investment risk. See WealthStep’s investment education videos for more on this topic, keeping in mind that inflation is a worse risk, often, in the long run, than market volatility.

With market volatility increasing after a period of high returns and low volatility after the Global Financial Crisis (don’t be surprised, that’s normal), it is a great time for you to review and confirm you have an appropriate savings rate and investment portfolio for your current stage of life, given your particular retirement readiness goals.

Notes: Stocks are represented by the Standard & Poor’s 500 Index. Bonds are represented by the Bloomberg Barclays U.S. Aggregate Bond Index. The hypothetical 50% stock/50% bond portfolio was rebalanced monthly. Data are provided by FactSet and cover the period from October 9, 2007 through June 29, 2018. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index. Sources: Vanguard calculations using data provided by FactSet, as of June 29, 2018.