Lessons from a flat tire – how to handle stock market volatility

Is recent market volatility making you nervous? Perspective could help you stay calm and on track.

Your financial journey is a lot like a car trip. On your route from point A to point B, while driving wisely, it is normal to experience stoplights, curvy roads, bad weather, or other elements that slow you down. A few times in your life, you might hit a pothole or nail that causes a flat tire. When you get a flat, your trip stops for a moment. Would you abandon the car and walk the rest of the way? Of course not! The whole car isn’t broken, so you would replace the tire with a spare and continue your journey. You know that if you fix the flat you will arrive at your destination sooner than if you walk.

People planning for retirement should take the same approach with their investments, especially if you’ve selected appropriate investments (i.e. using the right pre-built, diversified, asset allocation portfolio option for your long-term plans and life stage). On a financial journey, your portfolio is your car, and there will be big and small curves and economic storms that can temporarily slow your progress. If you remain a wise and disciplined investor and saver, it’s not about whether you’ll get to your retirement “destination.” Rather it’s about whether your arrival is delayed by circumstances you can’t control, just like the weather, or a flat tire.

Don’t worry, it’s normal to feel uncomfortable when the market experiences large drops but these fluctuations are a normal part of investing. However, panicking and dumping your long-term strategy is like running away or pushing your car off a cliff when you get a flat… you lock in the losses (it’s only a “paper loss” until you sell), and likely also miss the eventual recovery and gains; a big opportunity cost.

Those who don’t invest using a long-term plan, and/or not by life stage, tend to feel more panicky in rough markets, because it’s hard to stick with a strategy if you don’t have one.

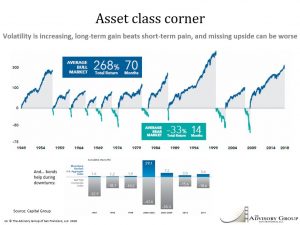

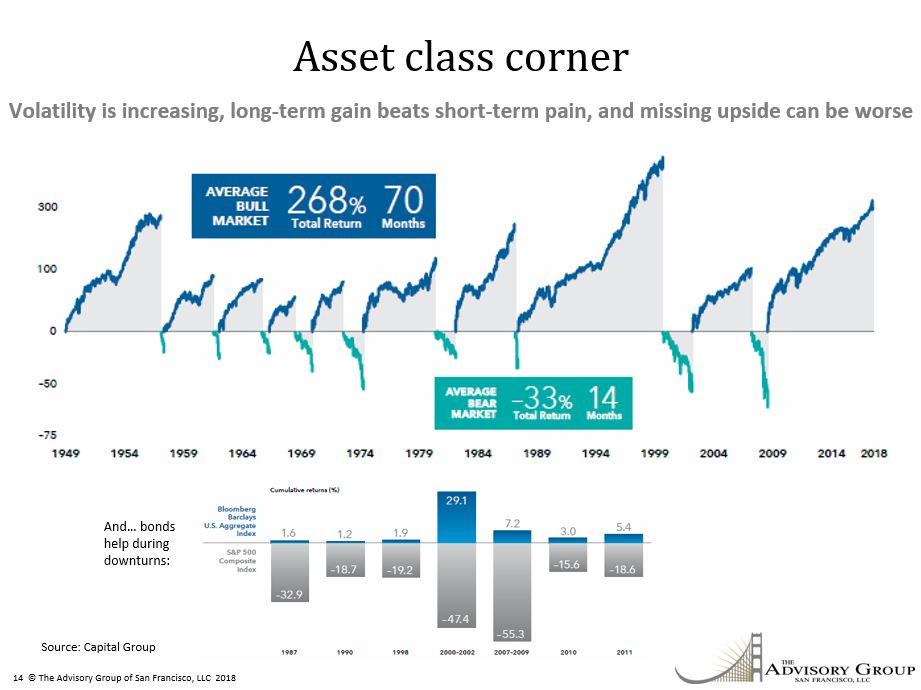

As of the end of December, some stock markets, especially those heavy in Technology stocks, have dropped about 20%, while other markets have fallen less. “Bear markets” like this are not uncommon, and typically bounce back within 18 months (see the up/down pattern in chart below, from our recent Quarterly Context video). What’s causing the current market volatility? Primarily, it is the cyclical yet unpredictable stock market “weather,” which is often driven by economic and political uncertainty. What makes the current market fluctuations more uncomfortable for some is that it is long overdue. The market has exhibited such low volatility in the last 6 years that many have forgotten that volatility is normal. In some cases, this is their first experience with negative markets.

It may help to remember that the market is simply an auction. If a few investors panic while others don’t want to buy or sell, that means there are few buyers, which may lead sellers to drop the price fast to attract buyers. Ultimately, it has to do with brain science… panic sellers are temporarily responding out of the fight or flight reflex (as if it the market were a life or death threat like a venomous snake), rather than deciding with the larger part of the brain that makes long-term decisions. That’s why some people later ask themselves… “Why did I do that, that wasn’t like the normal me!”

It may also help to remember that volatility can actually increase your wealth. If the market is down and you are adding money from your paycheck to your account, you are buying at lower prices. It’s as if the whole world is on sale! That’s what the wealthiest investors do, they make volatility their friend. As famous investor Warren Buffett once said, “The stock market is a device for transferring money from the impatient to the patient.” Ultimately, the question is… which group do you want to be in? The panic group or the profit group? It’s not always easy, but it is up to you.

Remember too, that getting out of the market and staying in cash is historically much riskier to your goals in the long run, due to the loss of purchasing power over time as you aren’t growing your assets sufficiently faster than inflation. Should you ever use cash? Yes, for the portion of your money you plan to spend in the near-term, generally 5 years from now or sooner.

So, remember, your portfolio is a car, not a snake, and volatility can be your friend. Stick with that mantra, and you’ll have success stories to tell in the long-run. If it would help you to read how similar past volatility was followed by market recoveries, here are a few past blog posts: volatility since the Global Financial Crisis, volatility earlier in 2018, and volatility in early 2016.